How to be financially fit in 2024

As we settle into the new year, it is an opportunity to reassess your financial health to help you start the year off...

READ MORE AU AU

AU AUPromoted by DuoTax

Depreciation is the wear and tear that occurs on items as time passes. As these items get older, the value of these items also decrease in value. This is what is known as depreciation. In the realm of property investing, these items are classified as either Plant and Equipment or Capital Works. The wear and tear of either plant and equipment or capital works in an investment property is called tax depreciation. Tax depreciation is the 2nd largest tax deduction that can be claimed after interest expense. Depreciation aids investors by allowing them to claim these tax deductions against their taxable income, thus providing increased tax refunds.

A Tax Depreciation Schedule is an ATO complying document that consists of two parts: Capital Works, also known as Division 43 and Plant & Equipment, also known as Division 40.

What is Capital Works (division 43)?

Also referred to by the Australian Tax Office as Division 43, it is the items that make up the building and those that are fixed to the building.

Here are some items that could depreciate part of the building:

|

Residential Built-in wardrobes Toilets and vanities Basins and sink Concrete slab Retaining wall and fences Timber framing |

Commercial Built-in workstations Car parking space Glass partitions Kitchenette Steel-framing of warehouse |

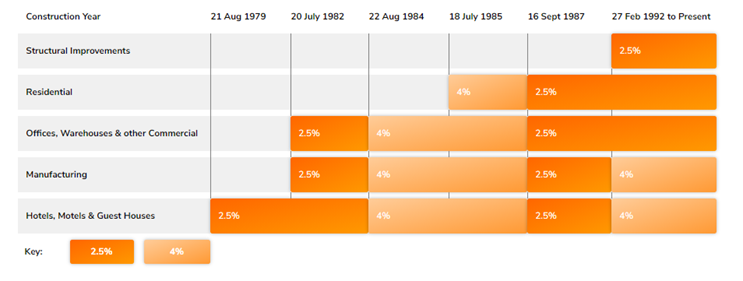

Which buildings qualify for Division 43 / capital works tax deductions?

There are a few questions that you can always ask an investor to answer this; When was the building built and what type of building is owned or leased? The table below shows the depreciation rate depending on the construction commencement year:

Equipment (division 40)?

Plant and Equipment are items that are easily removable from the property and most of the time, these include items that are motorised and have a shorter expected life span than the building (i.e 10 years effective life vs the capital works effective life of 40 years).

Plant and Equipment assets have differing rates of tax depreciation for both commercial and residential properties and is dependent on the ATO’s Effective Life Schedule which gives guidelines as to how many years the asset will last for, before its “effective life” is over.

Plant and equipment assets offer accelerated levels of depreciation, especially in the first few years of the schedule due to their nature of being faster to show wear and tear when compared to the bricks and mortar of a building. This means an investor can claim more immediately tax depreciation, typically within the first 5 years. The ATO then allows quantity surveyors to assess the value of these assets and include them into a tax depreciation schedule.

Here are some items that are considered plant and equipment:

|

Residential Oven Rangehood Air-conditioning units Smoke alarms Down lights Electric garage door & remotes |

Commercial Fire hydrant booster Billi hot water unit Door closers for door struts Coffee machine Warehouse cranes and hoists |

Which buildings qualify for Division 40 / plant & equipment tax deductions?

There are a few questions that you can always ask an investor to answer this; When was the building built and what type of building do you own or lease? Property investors who sign the contract for a purchase of a second-hand residential after 7:30pm on 9th of May 2017, are not eligible to claim depreciation on plant and equipment (division 40). These investors are still able to claim tax depreciation on brand new plant and equipment like carpet and air-conditioning units.

In summary, what scenarios are you eligible to claim depreciation?

Brand new residential properties

Buildings that still qualify for building depreciation (see division 43)

Second-hand properties that have had substantial renovations

Second-hand properties that have had minor renovations

Investors that purchase property in Managed Funds

Corporate entities that buy properties (e.g. Pty Ltd Company)

Second-hand properties owners who purchase new plant and equipment

Owners who switch from Principal Place of Residence (PPOR) to rental properties prior to 1st July 2017

You own a property that is not residential (commercial, manufacturing or motels)

If you are unsure whether you qualify for tax depreciation, it is as easy as sharing some property details with Duo Tax Quantity Surveyors on 1300 185 498.

As we settle into the new year, it is an opportunity to reassess your financial health to help you start the year off...

READ MORE

ADVERTORIAL: Presumably, overpaying for life insurance is the last thing you’d want to do. If you haven’t reviewed...

READ MORE

Promoted by NobleOak. Millions of Australians have life insurance within their super fund. This is sometimes known as...

READ MORE